SMSF vs Industry Super: Why SMSF balances are 300% larger at retirement

If you're serious about building wealth through superannuation, at some point you'll face a choice: stay in an industry fund, or set up a Self-Managed Super Fund (SMSF).

Both are legitimate paths. But they serve very different investors, and the difference in outcomes — especially for those who want to invest in direct property — can be significant.

This guide explains what separates them, what the data actually says, and how to know which one is right for your situation.

What Is an SMSF?

A Self-Managed Super Fund is a private superannuation fund that you control. You are the trustee. You decide what the fund invests in — shares, cash, property, bonds, or any combination of compliant assets. You also manage the compliance, reporting, and administration (usually with help from an accountant and auditor).

An industry super fund, by contrast, pools member contributions and invests them according to a pre-set strategy — typically a diversified mix of equities, fixed income, property trusts, and alternatives. Members choose a broad investment option (e.g. high growth, balanced) but have no control over individual asset selection.

Why SMSF Balances Are Often Larger at Retirement

ATO data consistently shows that SMSF members retire with significantly higher average balances than industry fund members. The reasons are structural, not accidental.

Investment control and customisation. SMSF trustees can invest in assets unavailable to retail funds — particularly direct residential and commercial property. A single well-chosen investment property inside an SMSF, held for 15–20 years, can produce capital growth that outpaces a diversified fund across the same period.

Lower fees at scale. Industry funds charge a percentage of your balance. At low balances this is fine — it's proportional. At high balances ($400,000+) the dollar cost becomes significant. An SMSF has largely fixed costs (accounting, audit, administration) that represent a smaller proportion of a larger fund.

Tax efficiency. SMSF trustees can manage capital gains timing, contribute non-concessional amounts strategically, and structure distributions to minimise tax in pension phase. Industry funds apply tax uniformly across the member pool.

Engagement effect. SMSF trustees are involved. They review performance, understand their assets, and make active decisions. Passive members in industry funds often leave unsuitable investment options unchanged for years.

When Industry Super Makes More Sense

An SMSF is not the right structure for everyone. Industry funds are the better choice when:

Your balance is below $200,000–$250,000. At lower balances, the fixed costs of running an SMSF (typically $3,000–$6,000 per year including accounting and audit) represent a higher percentage of your fund than most industry fund fees. The ATO recommends getting independent advice before establishing an SMSF with less than $200,000.

You don't want to be actively involved. Running an SMSF requires time, engagement, and some financial literacy. If you want a genuinely passive retirement savings vehicle, a well-chosen industry fund with a high-growth option is simpler and effective.

You have no specific alternative assets in mind. The primary advantage of an SMSF is asset control — particularly access to direct property. If you're happy with a diversified portfolio of listed assets, many industry funds deliver competitive returns without the compliance burden.

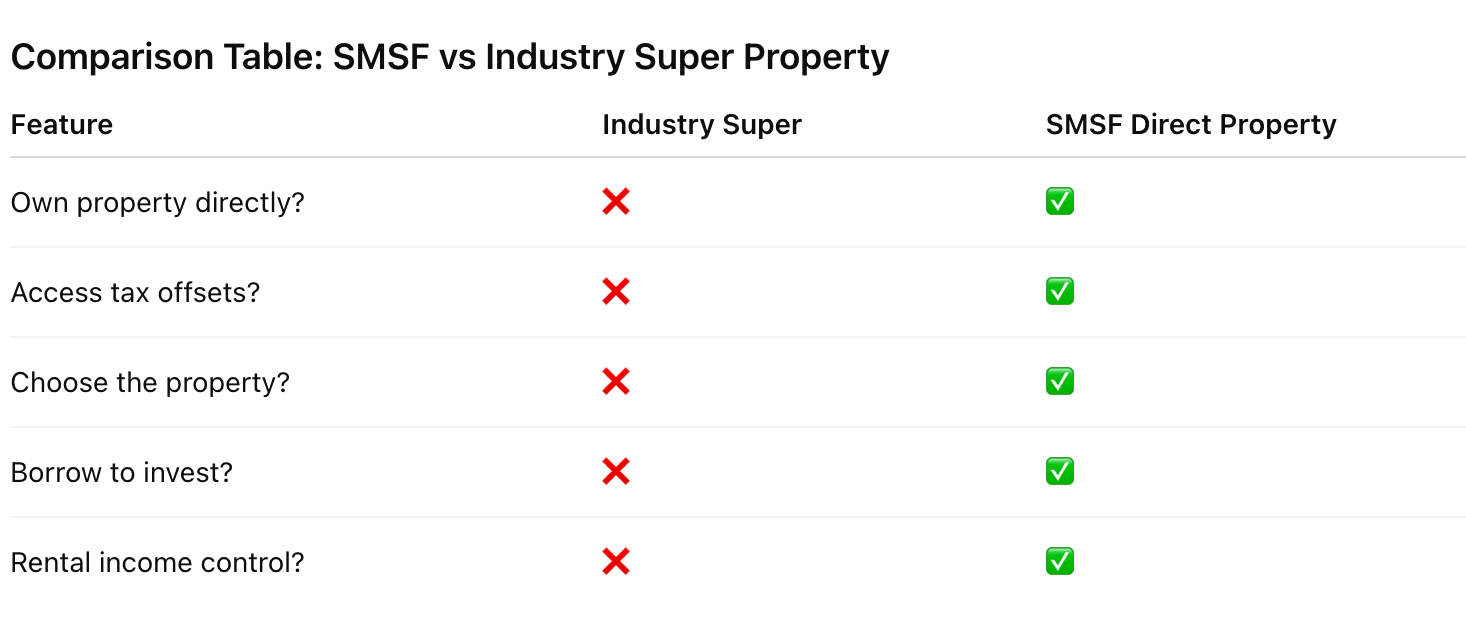

SMSF and Direct Property: The Key Advantage

The most significant reason high-balance investors move to an SMSF is to access direct property investment. Industry funds can hold property trusts (REITs) but cannot hold a direct residential property on behalf of a specific member.

An SMSF can borrow to purchase an investment property through a Limited Recourse Borrowing Arrangement (LRBA). The property must be purchased at arm's length and cannot be lived in by fund members or their associates, but it can be rented to unrelated tenants or (in the case of commercial property) to a related business.

Over a 15-year hold period inside a complying SMSF, a direct property in a growth market can deliver: capital growth taxed at 10% (in accumulation phase) or 0% (in pension phase), rental income taxed at 15% in accumulation or 0% in pension phase, and depreciation deductions that reduce the fund's taxable income.

For more detail on buying property through an SMSF: Buying Property With SMSF

For a breakdown of the specific tax benefits available: SMSF Property Tax Benefits

What to Look for in an Industry Fund (If You Stay)

Not all industry funds are equal. If you stay in an industry fund, the following matter:

Long-term net performance (after fees and tax). Superannuation Consumers Australia and APRA both publish comparative performance data. Look at 7 and 10-year net returns — not short-term numbers.

Fee structure. Total fee drag matters enormously over decades. 0.5% vs 1.0% in annual fees on a $500,000 balance is $2,500 per year — over 20 years that's $50,000+ in lost compounding.

Investment options. The default 'balanced' option often includes significant fixed income and cash that drags returns. A high-growth option (typically 80–90% equities) will generally outperform over a 15–20 year horizon for members still in accumulation.

For the broader property retirement strategy context: How to Retire Through Property in Australia: The Complete Strategy Guide

General advice disclaimer: This article is general in nature and does not constitute financial advice. Australian Retirement Office does not hold an Australian Financial Services Licence. Please consult a licensed financial adviser before making any decision about your superannuation structure.

Thinking About Property Inside Your Super?

Book a free 20-minute strategy call →https://www.ausretirementoffice.com/book

Download our free $200K Property Case Study →https://www.ausretirementoffice.com/book

Related reading: Buying Property With SMSF | SMSF Property Tax Benefits | Retire Through Property Australia

Conclusion

If you want average results, industry super works. If you want control, transparency, and the chance to accelerate wealth, SMSFs with direct property ownership are the way to go.

👉 Ready to compare your options in detail?

$997

$0

Get the Free ARO Investor Toolkit

Three free tools. See your net worth 10, 15 or 20 years out, find the highest-growth suburbs, and get your personal Property Number.

Takes under 2 minutes, No guesswork — just your numbers.

Real numbers. Your retirement. Free for a limited time.

YES — I want the free Investor Toolkit

At the Australian Retirement Office (ARO), our mission is simple: to help Australians retire better.

We believe retirement shouldn’t be left to chance or hidden inside industry super funds with limited control. For decades, Australians have built wealth through property, business, and smart tax strategies. That’s exactly what we help our clients bring into their super.

With a focus on clarity, control, and confidence, ARO provides education and strategies that put the power back in your hands, so you can retire on your terms.

www.ausretirementoffice.com.au